Pre-Underwriting Readiness Intelligence

See what FICO

can't see.

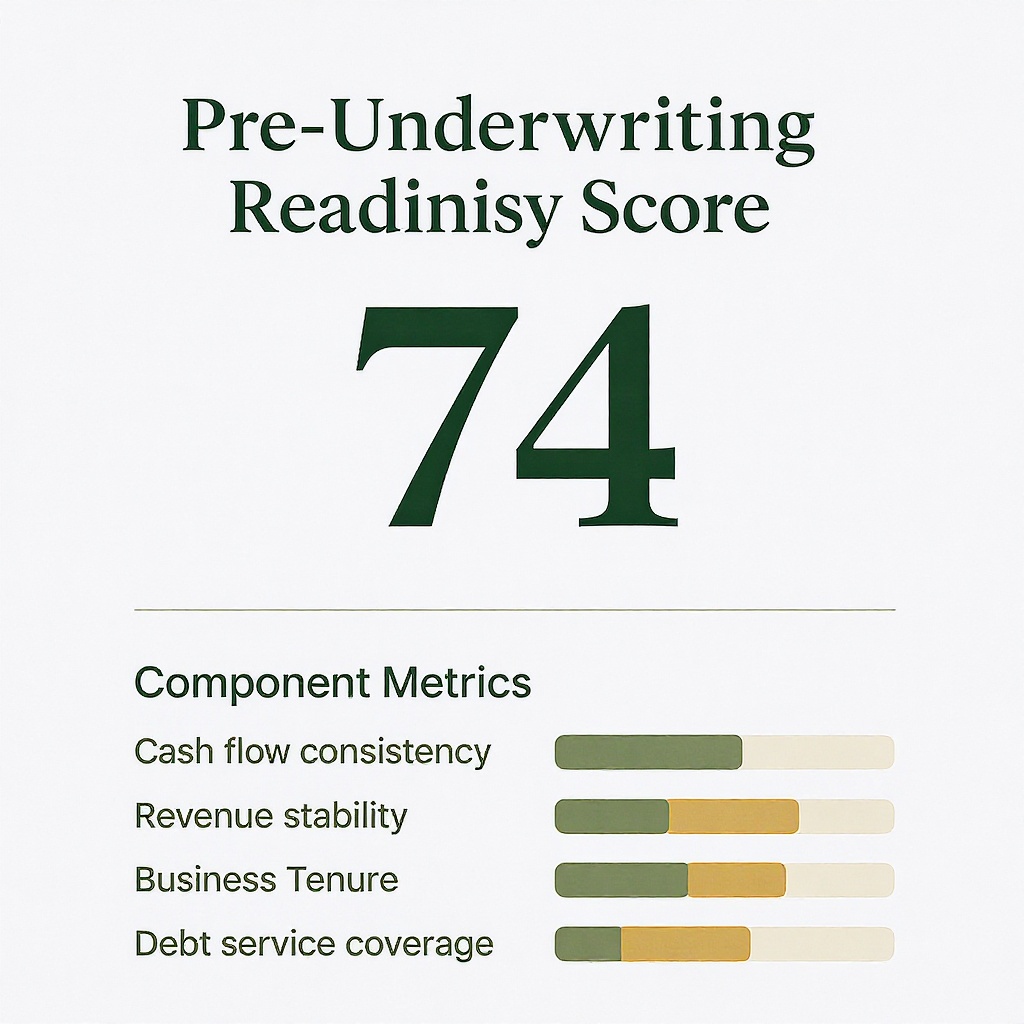

LendMark ingests 75+ alternative signals — cash flow, rent history, utility payments, business operating data — and produces a single 0–100 readiness score for every loan applicant. CDFIs, credit unions, and community banks use it to identify qualified borrowers faster and price risk more accurately.

75+

Alternative data signals

0–100

Readiness score, auditable

CDFIs

Credit unions, community banks